Articles

Welcome to our owl blog! This is where we expand important concepts and share exciting updates.

Latest article

London Calling: The UK’s drive to develop cryptoasset regulation

Following the EU’s introduction of MiCA earlier this year and legislative developments in the US with the GENIUS Act, other major jurisdictions around the world are steadily working to put in place clear rules of the road, intended to give both the cryptoasset sector and traditional finance clear guidance on how to make the most of blockchain technology. British politicians and regulators are working hard to develop regulation for the UK’s cryptoasset sector. Following a long-term political commitment to develop the UK into a ‘global crypto hub’, the regulatory pieces are beginning to fall into place to make this happen. When this regulatory framework has been implemented, the UK will (if all goes to plan) have rules that support the steady growth of the sector and innovation in finance and technology - alongside stronger consumer protection and market stability. In this Owl Explains post we outline the different recent milestones the UK has passed, and look ahead to what is coming next. HM Treasury: Draft Statutory Instrument for a Regulatory Regime for Cryptoassets HM Treasury (the UK government’s Ministry of Finance) published its so-called Secondary Legislation for cryptoassets on 29 April 2025. Secondary Legislation (via a ‘Statutory Instrument’) is a piece of more detailed legislation that follows on from higher-level, overarching legislation that has already been passed by both Houses of Parliament; in this case, comprising the 2023 amendment to the Financial Services and Markets Act (FSMA), which now brings. cryptoassets into UK financial legislation. The proposed Statutory Instrument defines ‘qualifying cryptoassets’ and ‘qualifying stablecoins’ as regulated ‘specified investments’and brings under FCA oversight key activities such as running crypto exchanges and custody services, dealing, arranging, staking, and issuing stablecoins. The proposal also amends money‑laundering and financial‑promotion rules, and ensures that stablecoins don’t unintentionally fall under other categories like e‑money or collective investment schemes. Decentralized systems without a controlling party are broadly exempt, and there would be a transition period to allow firms to apply for authorisation. FCA DP 25/1: Regulating cryptoasset activities Shortly after HM Treasury published its proposals for the Statutory Instrument, the UK’s main financial regulator, the Financial Conduct Authority (FCA), published its related Discussion Paper (DP) 25/1 on Regulating cryptoasset activities. The discussion paper builds on existing financial market rules, proposing that crypto trading venues follow similar standards to traditional trading venues, with strict transparency requirements, conflict-of-interest rules, and protections for retail clients. It also suggests that intermediaries should follow best-execution rules, that payment-for-order-flow is banned, that lending and borrowing to consumers may be heavily restricted, and proposes a prohibition on the purchase of cryptoassets using credit cards. With respect to staking, clear disclosures, customer consent, separate wallets, and liability safeguards are proposed. Truly decentralised systems without a controlling party remain outside the framework, but any service deemed by the FCA to have a central operator would be included. FCA CP 25/14: Stablecoin issuance and cryptoasset custody Later in May 2025, the FCA launched Consultation Paper (CP) 25/14, proposing rules for the issuance of fiat-referenced stablecoins and the safe custody of cryptoassets. Issuers would need to fully back every stablecoin with high-quality, liquid assets held in a statutory trust via an independent custodian, honor redemptions at par value within one business day, and regularly publish transparency reports on reserves and redemption policies. Meanwhile, crypto custodians would be required to segregate client tokens from their own, maintain accurate records and governance, and hold assets in trust. This adapts established FCA protections from traditional finance for the digital asset sector. FCA CP 25/15: A prudential regime for cryptoasset firms At the same time as CP 25/14, the FCA published CP 25/15 to propose a dedicated prudential rulebook for crypto firms that issue fiat‑backed stablecoins or safeguard cryptoassets. It proposes two new rulebooks: COREPRU, which covers general capital, liquidity, and risk standards, and CRYPTOPRU, which is tailored to crypto activities. Firms will have to hold the greater of three capital measures: a permanent minimum (£350,000 for stablecoin issuers, £150,000 for custodians), a buffer equal to 25 % of fixed overheads, or an activity‑based “K‑factor” (equivalent to the market value of 2 % of stablecoins issued or 0.04 % of cryptoassets safeguarded). On top of that, liquidity rules require crypto firms to set aside enough in high‑quality liquid assets to cover short‑term obligations and ensure resilience, plus safeguards on concentration risk to avoid over‑reliance on any single counterparty or asset. Further proposals by the FCA are expected in the coming months, following its clear and scheduled ‘Crypto Roadmap’. Taken together, the Roadmap aims to build trust and stability in crypto markets ahead of final rules that are expected to be published in 2026. The rules will then come into effect some time in 2027. What does Owl Explains think about these proposals? Owl Explains strongly supports the UK’s efforts to develop its regulatory regime for cryptoassets. As we consistently argue, a clear, stable and proportionate set of rules is needed - right around the world - to allow the long-term development of blockchain technology and ensure that its benefits can be fully realized. Piece by piece, policy-makers are laying the groundwork for this in the UK. For us, the key thing is that regulators recognise that infrastructure providers on blockchain networks are not in themselves financial intermediaries, including but not limited to when they use native DLT Tokens to perform technology functions integral to the operation of the blockchain. The recent proposals put forward by HM Treasury and the FCA go some way to acknowledging this, but it will benefit everyone to have that point clarified more explicitly. You can read Owl Explains’ Response to the FCA’s DP 25/1 here. And be rest assured, as the FCA follows its Crypto Roadmap, we’ll keep on highlighting what it means and making the case for a clear, stable and proportionate regulatory framework for cryptoassets in the UK - and around the world.

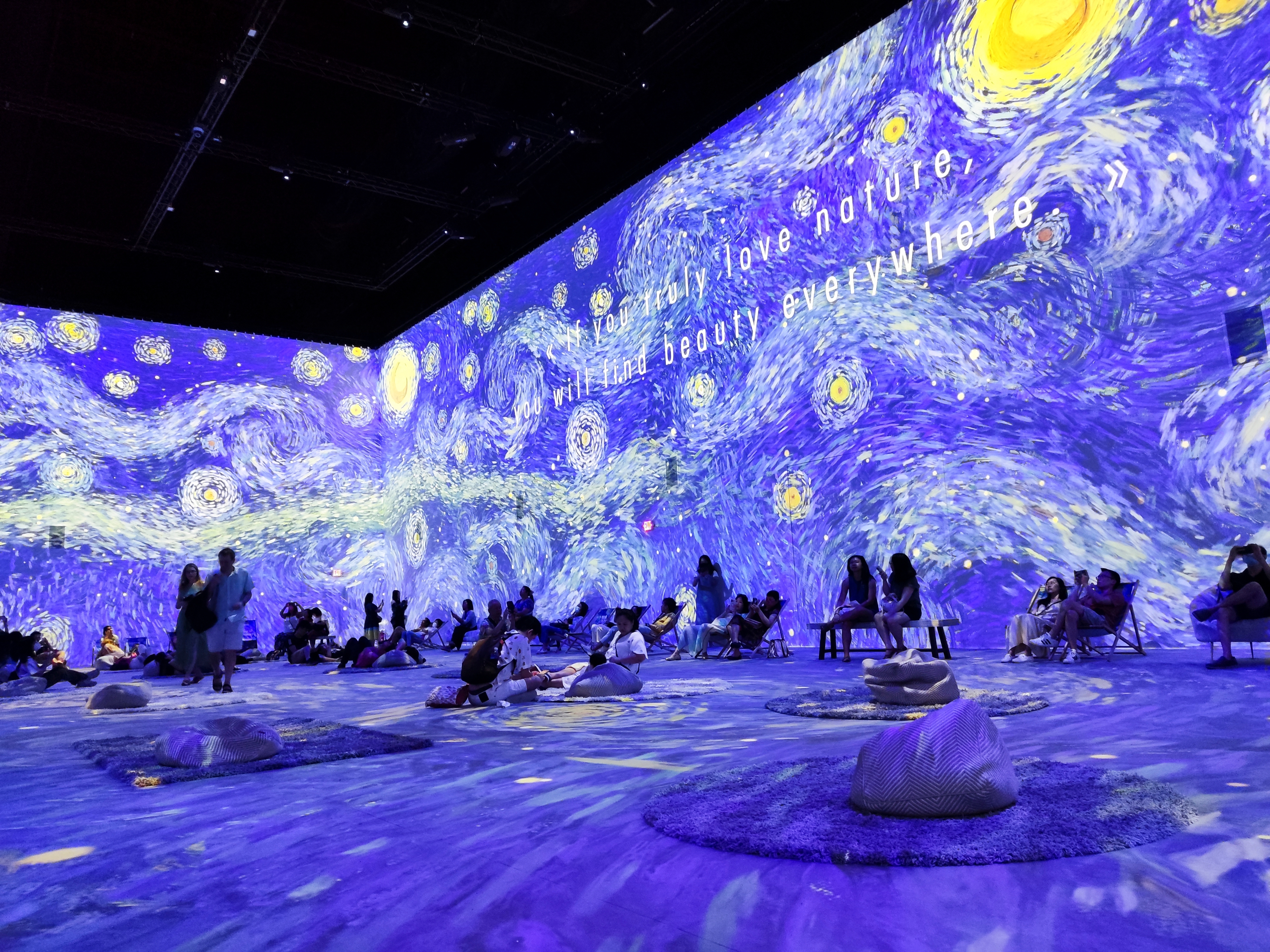

Future Forward: Key Themes from the Owl Explains Crypto Summit

What better place to explore the future than a setting steeped in the past? Against the backdrop of the Dorchester Hotel—an iconic London venue rich with history and elegance—the first Owl Explains Crypto Summit brought together a dynamic mix of policymakers, technologists, legal minds, and industry leaders to tackle some of the most forward-looking questions in crypto and digital markets. The turnout was strong, the energy high, and the conversations —both on and offstage — were substantive. This wasn’t a day of soundbites or sales pitches! So in between the delicious food (miniature vegan lemon meringue pie, yes please), getting your new complimentary professional headshot from Van Scoyoc Associates, and enjoying the contents of your OE tote swag - our owlet attendees were able to enjoy a range of panels, delving into topics including privacy, liquidity, global commerce, autonomous code, anti-money laundering and tokenization. Big Picture Perspectives Sprinkled delightfully among our roundtables we were able to hear from three keynote speakers whose leadership continues to shape digital policy at the highest levels: Lord Holmes (UK House of Lords), Peter Kerstens (European Commission), and MEP Ondřej Kovařík (European Parliament). While occupying very different roles in the policy ecosystem, they all spoke to the power of blockchain and digital assets to enhance the global financial world of tomorrow. Lord Chris Holmes emphasized the need for thoughtful regulation of emerging technologies and called for a cross-sectoral AI framework—highlighting both innovation and social inclusivity, especially for sensory-impaired communities. Peter Kerstens, “the father of MiCA”, used his keynote to underline Europe’s new crypto-assets framework and urged developers not to wait for prescriptive regulation, but to innovate, demonstrating in practice how the rules can be shaped and applied. MEP Ondřej Kovařík offered a forward-looking view on MiCA implementation and its broader implications for the European crypto ecosystem, emphasizing the importance of ensuring a smooth and coordinated rollout of the new framework. With those big-picture perspectives anchoring the day, we can now zoom into the practical, the technical, and the sometimes provocative. Across six expert-led roundtable sessions, attendees had the chance to get stuck into the details: asking hard questions, sharing lived experience, and debating what’s really needed to take this industry from potential to practice. Roundtable Session 1: Tokenizing It All The summit’s first roundtable, Tokenizing It All, explored the implications of a fully tokenized world where stablecoins are commonplace with panelists Helen Disney, Sean McElroy, Yuliya Guseva, Jannah Patchay, Varun Paul, Isadora Arredondo, and Kene Ezeji-Okoye. The discussion delved into the fundamentals - what does it mean to tokenize something, the practical challenges and opportunities of tokenizing various asset classes (including Sean’s apartment!), the role of regulation, and the potential impact on commerce and trading. Roundtable Session 2: DeFi-ing Liquidity The second session, DeFi-ing Liquidity, examined the dynamics between decentralized and centralized finance in providing market liquidity. Panelists Fahad Saleh, Lavan Thasarathakumar, Joey Garcia, Dan Gibbons, David Wells, Sara George, and Olta Andoni had an animated discussion, highlighting the benefits and risks associated with DeFi, the need for regulatory clarity, and the future of liquidity provision in a tokenized economy. And even a sprinkling of friendly feather ruffling as the question of definitional prowess between academics and lawyers came to a head! Roundtable Session 3: Globalizing Commerce If the audience were hungry, they weren’t letting it show. The high spirits continued into the final panel of the morning, which addressed the complexities of global commercial structures in the context of tokenized assets. Panelists Yesha Yadav, Erwin Voloder, Scott Mason, Sam Gandhi, Emma Pike, Dagmar Machova, Ari Pine, and Amanda Wick discussed jurisdictional challenges, the convergence of commerce and trading, and the legal implications of cross-border transactions in a blockchain-enabled world. Roundtable Session 4: The Chase is On The afternoon discussions kicked off with a great panel looking into enforcement, litigation, and anti-money laundering in the realm of tokenized and decentralized finance. Our expert panel featuring Justin Gunnell, Christopher Mackin, Sayuri Ganesarajah, Joanna F. Wasick, Laura Clatworthy, Isabella Chase, Joe Hall, and Jesse Overall shared insights on tracking illicit activities, the role of international cooperation, and the evolving legal landscape in digital finance. They also touched briefly on the rise of wrench attacks, which involve real-world violence targeted at individuals for their digital assets - reminding our audience that the digital and physical worlds are now inextricably linked. Roundtable Session 5: When We Need Secrets The fifth roundtable raised some interesting Nuggets (!) on privacy and identity in a fully tokenized and decentralized market. Speakers Seema Khinda Johnson, Dr. Agata Ferreira, Adam Jackson, Eugenio Reggianini, Adi Ben-Ari, Peter Freeman, and Chris Grieco debated the challenging balance between giving citizens control and privacy, and combating fraud. They discussed the development of digital identity solutions, and the ethical considerations of data protection in blockchain applications. Roundtable Session 6: Code Running Solo Last but by no means least, the final session, Code Running Solo, explored the intersection of cybersecurity, artificial intelligence, and autonomous code in tokenized markets. Panelists Lilya Tessler, Norma Krayem, Laura Navaratnam, Fabian Schär, Eva Wong, Joni Pirovich, and Caroline Malcolm examined the challenges of securing decentralized systems, the implications of AI-driven decision-making and the role of regulation (on which opinions differed wildly!) within that. Looking Ahead: A Community with Purpose As Wee Ming Choon took to the stage to close out the first ever The Owl Explains Crypto Summit, the mood was buoyant, especially for a conference ending after 6pm! This wasn’t just a policy event—it was a community coming together to explore real questions about how our digital future is taking shape. One topic that kept coming up was regulation. Are regulators getting it wrong because they have turned their back on technology and competition? Or is that a mischaracterization of the role of regulation - and in fact the incentives work against regulators, promoting continuity of the status quo? Our panels on liquidity and autonomous codes in particular discussed this at length - and while this is not a discussion that can be solved easily, creating platforms for smart and articulate individuals with a range of views and experience to debate them can only serve to be a step towards answers. As our Owl Explains parliament retired to the drinks reception, brains fizzing with a heady mix of topics - from tokenization to AI, from privacy to liquidity, all conversations that didn’t shy away from complexity. And that’s exactly what made them so valuable. In the words of Owl Explains founder Lee Schneider, “I came away with a really positive sense that we will change the world.” It was a sentiment shared by many in the room: pride in what’s been built, and excitement for what comes next.

Tokens, Currencies, Coins, Assets… What the Heck Are We Talking About Anyway?

“Stablecoins are a type of cryptocurrency that act as a form of cash but sit outside the banking system. They are used to pay for other crypto assets…” Financial Times, 2 April 2025 There are a lot of names in the crypto space. People often use them interchangeably. Different countries, different companies, and different regulators all have their preferred names for what they’re talking about. But it matters that we all know what we’re talking about when we use these words and - as much as possible - use them in the same way. This is particularly true when it comes to regulation because without solid definitions, compliance is difficult. In this Owl Explains note we’re going to tackle lexicography for commonly used terms for what we prefer to call tokens. And explain why we think ‘tokens’ is the best word to use when talking in a general sense. By the end of the article you should be able to see how the Financial Times quote at the top uses these different terms - and decide whether you think it gets them right. Crypto: Let’s start with the fundamental word: ‘crypto’. The ‘crypto’ in cryptoasset or cryptocurrency comes from ‘cryptography’. That is, the use of codes or ‘encryption’ to provide secrecy. Cryptography is an ancient practice going back many thousands of years, at least to the ancient Egyptians. Modern cryptography has been greatly enhanced by the use of computers and new techniques. Together these allow people to create the public and private keys necessary for blockchain. The use of ‘crypto’ essentially just means that some information has been ‘encrypted’ using these modern cryptographic techniques. And in practice it is used to refer to something on a blockchain - or the whole blockchain-based sector itself. Cryptocurrency: A cryptocurrency is, naturally enough, a type of currency utilizing ‘crypto’. But what is a currency? A currency is a type of money widely used in a particular area. It is a form of ‘money’. So by calling something a ‘cryptocurrency’, its founders are implying that it has the characteristics of money: the dollars, pounds, euros or yen that you use every day. The three fundamental characteristics of money are: That it is a store of value. That is, that what you hold today will be worth the same amount tomorrow. That it is a means of exchange. That is, that other people will be happy to take it in exchange for goods or services they provide. That it is a unit of account. That is, that you can price a good or service in it. While ‘cryptocurrency’ was one of the first ways of describing these blockchain-based units, it is now largely out of favor since many (or even most) don’t fulfil these three characteristics. When was the last time you heard someone price something in Dogecoin? Cryptoasset: More popular nowadays is the term ‘cryptoasset’ (and note that there are different ways of spelling this: all one word, with a hyphen, or as two separate words). But what’s an asset? An asset is something that has (financial) value. So a cryptoasset is something on the blockchain that holds (or represents) value. This makes sense as a term, given that many people buy or sell ‘cryptoassets’ as speculation (to make money) or because it offers them access to something else that has value (like a blockchain protocol or a good or service in the real world). But while this is a useful term that is in wide use, it does also have one issue with it: it implies the crypto ’asset’ does have some sort of value. Which they don’t always. For example, a tokenized digital record, such as a diploma, might not ever have (or be intended to have) a value. So calling them ‘cryptoassets’ would imply a use - and therefore a form of regulatory treatment - that doesn’t make sense. This is one of the reasons we stress token classification, including in our submission to the SEC Crypto Task Force. This terminology matters when it comes to thinking about the correct regulatory treatment for things on the blockchain. Nowadays when a regulator or government official says ‘crypto’ they’re referring to a cryptoasset - and probably including the idea of a ‘cryptocurrency’ within it. Stablecoin: Stablecoins are a unique type of ‘cryptoasset’ that attempt to maintain a stable value against a reference asset. Usually today this reference asset will be a so-called ‘fiat currency’: in other words, the normal currency of any given country (dollars, pesos, etc.). In this sense they are a ‘crypto’ or on-chain representation of normal money that already exists, and they fulfil the three functions of currency by ‘piggybacking’ on the underlying existing fiat currency. Previously (around 2018-2019) the term was used more loosely to mean something that tried to reduce volatility in the value of a cryptoasset - either through its backing asset or via an algorithm. Now, largely driven by regulation, ‘stablecoin’ tends to only refer to a token that is pegged one for one to a single fiat currency, or perhaps sometimes to a group (a ‘basket’) of different fiat currencies. So depending who you’re talking to, ‘stablecoin’ could be referring to the whole universe of ‘stablecoins’ that attempt to minimise volatility or just to those, more common now, that maintain a stable value against the reference asset or fiat currency. Central Bank Digital Currency (CBDC): A CBDC is very similar to a stablecoin, in that it is the ‘digital’ version of a fiat currency, except that it is created by a government’s Central Bank or other monetary authority. That is, a CBDC is issued by a country’s public sector and is a direct liability of that authority. There is therefore no private sector company responsible for it, or which could go bankrupt or fail to provide it. That makes it very safe, in an economic sense, for people who hold it. Many countries are still exploring developing a CBDC, and there are significant ongoing political discussions around questions like privacy rights and the ability of governments (or Central Banks) to control how a CBDC might be used by citizens and businesses. Digital [currency/asset/cash]: As you’ll have seen in the term CBDC, this is not called ‘crypto’ but ‘digital’. That’s because ‘crypto’ implies something on a blockchain, as we’ve seen, and through its meaning about the wider sector still sometimes has a negative connotation. Central Banks don’t want to be associated with that - and anyway may not issue on a blockchain. So they used ‘digital’. That makes sense as far as it goes, but has one major problem: the overwhelming majority of ‘traditional’ money is also digital because it exists as commercial bank deposits (and indeed as Central Bank reserve deposits). These deposits are purely digital in that the value solely exists as information inside bank computers. Calling something blockchain-based as ‘digital’ does not really help distinguish it. In other words, digital is a much broader category that includes crypto. Virtual [currency/asset/cash]: Some people use the term ‘virtual’ in an attempt to get around this confusion, though it’s now a little less used than it used to be. ‘Virtual’ covers basically the same ground as ‘digital’ but without the confusion about existing bank deposits. In this sense it’s really used as a synonym for ‘on-chain’: that is, something based on a blockchain. Virtual has more traditionally been used to mean anything on the internet, such as people referring to a “virtual meeting” when they do a video call. For these reasons, by and large the term ‘crypto’ is winning out as the main usage for something on-chain. All these terms are in use, but all have problems. So what does Owl Explains use? Well, we prefer the term ‘Token’. This word refers to something that is used to represent an asset, item, bundle of rights or thing. It does not necessarily imply financial value (like ‘asset’) or money (like ‘currency’). It is technology neutral, so does not imply something has to be blockchain-based (like ‘crypto’) or not (like a CBDC) - and indeed it even applies to non-digital/virtual representations like those that are based on paper (like old time stock certificates or tickets to an event) or metal (like subway tokens). A ‘token’ can refer to all these things without implying any characteristic, and therefore without prejudging any regulatory treatment. And the word ‘token’ allows anything to be ‘tokenized’ or ‘represented by a token’, which is a major growth area for the blockchain sector at the moment. In an upcoming post, we’ll explain how tokens themselves can be classified from a regulatory and market point of view.

Exploring Models of Staking

This is Part Two in our Staking series. Click here to read Part 1. Staking is frequently a mischaracterized and misunderstood activity, in large part due to a lack of understanding surrounding the fundamental principles of staking as well as the different models. Staking is an integral part of the infrastructure that keeps a blockchain functioning and secure. It is a technological activity utilizing hardware and software, and reliant on communications over the internet. It determines who participates in the updating of the blockchain to maintain Byzantine fault tolerance. It does not require the participant to transfer ownership of their tokens to a third party - it is not lending or custody —but some models do involve the token owner transferring control. While rewards are in place to act as an incentive for participants to stake their tokens, this is an outcome of the process, not the driver for it. PoS includes several variations, each catering to different user needs and blockchain architectures. Solo or Direct Staking Users run their own validator nodes via their own software and hardware, maintaining full control over their staked assets and potentially receiving higher rewards than if they were using a third party. However, the barrier to entry for solo staking is high - there is significant technical expertise required as well as a large up front equipment cost. Additionally, there is the cost of the stake that must be posted: 32 ETH to activate a validator on Ethereum, 2000 AVAX on Avalanche, for example. Users are solely responsible for maintaining hardware uptime and security, and therefore will bear the full effect of any penalties from the protocol if there are failings. Third party models The term Staking-as-a-Service (StaaS) is often used very broadly in the blockchain ecosystem, but is actually not particularly helpful, as it is too generic a description. A third party can manage many different aspects of the staking process for users depending on a number of factors; it is best therefore to split this category out. Non-custodial delegated staking: Token holders stake their cryptoassets via a self-hosted wallet but delegate validator operation to a third party, such as a StaaS provider, in exchange for a service fee. This reduces costs and technical complexity compared to solo staking while ensuring that only the token holder can sign transactions, claim rewards, and unstake using their private keys. Custodial delegated staking: many large cryptoasset custodians now offer staking as an ancillary activity. The custodian stakes the tokens (with permission) on behalf of the token holder in exchange for a service fee. While the third party will take custody of the assets in this example, it is because of their nature as a custodian, not because staking requires it. Custodians can store the tokens in different wallets based on the requirements of the tokenholders: segregated staking keeps the tokens entirely separate from others and there is no co-mingling of assets; omnibus staking puts all tokens together in an omnibus or aggregated wallet, lowering the barrier to entry; pooled staking combines assets across multiple participants in return for a ‘share’ of an already active staking position. Liquid Staking: A commonly cited concern with staking is that once a token is staked to the network, it can’t be accessed until the end of the lock up period. Liquid staking providers allow tokens to be deployed via a protocol to receive a receipt token (or Liquid Staking Token (LST)) which acts as proof of the underlying staked tokens and any associated rewards. The LST can then be deployed in other activities e.g. on Defi protocols and can continue earning rewards. Staking isn’t a one-size-fits-all approach—different models cater to different needs, from solo staking for those who want full control to third-party and liquid staking options that lower barriers to entry. That’s why it is important to read the fine print on whichever model you choose. While these models make staking more accessible and flexible, they also come with varying degrees of risk, from slashing penalties to counterparty exposure. So, what should you watch out for when staking your assets? In our final post, we’ll explore the key risks and considerations to keep in mind before getting started. Stay tuned!

The Fundamentals: What is Staking?

Welcome to Part 1 of our Staking Series... Consensus mechanisms serve as the backbone of decentralised networks, ensuring security, efficiency, and trust in the evolving landscape of blockchain technology. In recent years, Proof of Stake (PoS) has emerged as an energy-efficient alternative to Proof of Work (PoW), becoming one of the most widely adopted consensus mechanisms today. Unlike PoW, which relies on computational power, PoS leverages token ownership to validate transactions and secure the network, reducing energy consumption while maintaining security and decentralisation. Staking - A Brief History and Explanation A consensus mechanism is exactly as it sounds - a means of reaching agreement between network participants. In the absence of a centralized intermediary that can review and verify transactions, as well as monitor participants, decentralised networks need to build trust and reach consensus through other means. This is also known as the Byzantine Generals problem. Proof of Work (PoW) was the first widely adopted consensus mechanism, and supports tokens like Bitcoin - it actually originated in the early 1990s as a way of preventing email spam. Miners compete to find a valid cryptographic hash that meets the network’s difficulty target. The first miner to succeed proposes a new block of transactions and if the network verifies the block as valid, it is permanently added to the blockchain. The successful miner receives a block reward (newly minted tokens + transaction fees). PoW makes fraudulent transactions extremely difficult, because it requires huge amounts of computational power to execute a 51% attack (controlling the majority of mining power). However, PoW has faced criticism as the growing number, diversity, and value of PoW networks and their cryptocurrencies have led to a significant increase in computational power demands, reaching levels comparable to those of mid-sized countries. Proof of Stake (PoS) has been developed as an alternative consensus mechanism, aiming to achieve the same level of network security but without such high energy demands. Unlike the outright competition of proof-of-work, proof-of-stake (PoS) uses a different set of incentives to make sure that network participants behave honestly. PoS relies on participants—known as validators—to lock up, or "stake," their tokens in order to propose and validate new blocks. Validators, like miners, provide technology services to the blockchain. They run software to implement the consensus and validation process. They operate infrastructure hardware and software (akin to Internet service providers). Both miners and validators have a critical role in recording information to their respective blockchains and enabling decentralized systems, but they do so differently. Validators are selected based on the size of their stake and other network-specific criteria, rather than engaging in energy-intensive computational puzzles as seen in PoW. The more tokens a participant stakes, the higher their chances of being chosen to validate the next block. However, this selection process is often weighted with additional mechanisms to prevent undue centralization. When a validator is chosen, they are responsible for verifying transactions, adding new blocks to the chain, and ensuring the overall integrity of the network. In return for their services, they receive staking rewards in the form of newly minted tokens and transaction fees. As shown by the explanations above, PoW and PoS are not actually the core of how validation of transactions and consensus about adding blocks are achieved. Rather, they are the mechanism by which the participants in those activities and the proposers of blocks are permissioned by the network. This is known as “sybil resistance” because it stops attackers from gaining easy access to these very important functions by imposing a cost to participate. Validation of transactions and consensus about which block to add next are carried about by the miners and validators who have paid the price of admission through their work or their stake. Staking market today PoS has demonstrated its ability to strengthen network security while also being significantly more energy efficient. Additionally, unlike PoW which requires significant upfront investment, PoS allows a broader range of participants to contribute to network security. In a PoS system, validators are selected based on the amount of cryptocurrency they stake rather than computational power, which means that individuals and organizations with varying levels of resources can participate without needing expensive mining rigs or access to cheap electricity. As such, PoS blockchains have evolved quickly over the past few years, accompanied by an increase in staking activity. In Q1 2024, the average staking reward was 10%, translating to annualized staking rewards of $14 billion—up from $4.9 billion in the same quarter of 2023. The total value of staked assets during this period was projected to reach $239 billion. Staking has come a long way, offering a more energy-efficient and accessible alternative to traditional mining. As the market continues to grow, understanding the different models of staking becomes essential for both newcomers and seasoned participants. So how do different models compare, and what are the trade-offs between them? Stay tuned for our next post, where we’ll break down the various staking models and what they mean for investors, networks, and the broader crypto ecosystem. Part 2 available now! "Exploring Models of Staking"

From Wild West to Foundation of Finance: The Case for Public Permissionless Blockchains

As recently as three or four years ago, if you were a central bank, financial institution or large enterprise wanting to experiment with blockchain technology, it would be a no-brainer to choose a private, permissioned network. Public permissionless blockchains were - and in many cases still are - viewed as a Wild West of DeFi lawlessness and NFT-driven hedonism. However, the tide is rapidly turning, and in the past couple of years we’ve seen increased interest from banks in building on public blockchain. Even the Bank for International Settlements - the ‘central bank of central banks’ - has started to run projects built on public blockchain! In this article we’re going to explain what public permissionless blockchains are, the benefits they can bring, and some examples of how financial institutions are already building on them. We’ll then look at why so many people in both the public and private sectors have historically been inherently against public permissionless blockchains, what’s changing in terms of both technology developments and public perception, and how the barriers previously perceived by regulators and regulated entities are being broken down. But first, let’s start with a few definitions. What do we mean when we say "public" and "permissionless"? Public blockchains are open and accessible to anyone. Anyone can join the network, view the ledger and validate transactions, without any restrictions. In this respect, they’re fully decentralized and self-governing, and have a high degree of autonomy and resilience. Permissionless means that there are no gatekeeping requirements associated with access to and participation in the blockchain, and nobody needs special permission in order to join, validate or develop applications on the network. While these terms often overlap, they are not entirely synonymous. A blockchain can be public but not entirely permissionless if, for example, only authorized nodes can validate transactions (as in some ‘hybrid’ models, like Hedera). Conversely, a permissionless blockchain is typically public, as it relies on open participation to maintain its decentralized ethos. But taken together, these qualities underpin the trustless and open nature of many blockchain systems, enabling broad participation. What are some of the benefits of public permissionless blockchains? Public permissionless blockchains don’t rely on a central authority exercising power and control to create trust between unknown counterparties. The ‘trust’ in this instance comes from the combination of decentralization, robust consensus mechanisms and economic incentives, cryptographic security, transparency and immutability of public blockchains. This decentralization eliminates single points of failure, making these networks more resilient against outages or cyberattacks. Open access allows global participation, enabling a broad range of developers and institutions to build and integrate applications, driving innovation, liquidity, and diverse use cases through composable ecosystems. Network effects also play a role. The larger and more established a blockchain's user base, the more secure and trustworthy it becomes. This is because a larger network typically has more nodes validating transactions, making attacks less feasible. Public blockchains also often rely on open-source software, allowing the best developers and security experts globally to test, audit and improve the code. This open scrutiny helps identify vulnerabilities and maintain robustness. For the blockchain community, it’s axiomatic that all this is better: safer, more reliable, more universal. Permissioned networks are still great for certain applications, particularly those in which there are a limited number of participants who all need to be on-boarded and known to each other, implementing a very specific use case and with no need to interact with a broader range of participants or assets. But there’s an increasing recognition of the benefits that public permissionless blockchains bring for asset tokenization: distribution and liquidity, the benefits of a diverse ecosystem, and other network effects. Why and how are regulated financial institutions starting to use public blockchain? Issue an asset on a private permissioned network and it’s available only for the use case implemented on that network, and to the participants in that network. Issue onto a public permissionless blockchain, and your tokenized asset can be accessible to any participant. It can be exchanged bilaterally between wallet-holders, picked up and integrated into decentralized exchanges or used as collateral in lending protocols. Users can pay for them in any stablecoins available on the network, or swap them directly for other tokenized assets. It can also be composed with other tokenized assets into use cases and applications that you as an issuer might never have foreseen. It can be bridged onto other public permissionless blockchains and made available to their ecosystems. All of this distribution capability drives greater liquidity and innovation - and that’s evidenced by the growing trend towards tokenized fund issuance on public chains. A growing recognition of these benefits - alongside all the other benefits of the technology - is fueling more experimentation and a growing cohort of live projects on public chains. Some high-profile examples include: A set of institutional players, including T. Rowe Price Associates, WisdomTree, Wellington Management, and Cumberland, partnering to tokenize assets and build trading and other applications on Avalanche Spruce. Citi’s FX pricing and execution solution for Project Guardian. Citi’s exploration of tokenized private market funds. Membrane Finance’s launch of the first Mica-compliant Euro stablecoin. Franklin Templeton’s tokenized money market fund, BENJI. DTCC’s Digital Asset Launchpad sandbox, as well as its Smart NAV pilot. JP Morgan’s Kinexys blockchain infrastructure for tokenized investments and cross-border payments. Standard Chartered and Ant International blockchain-based settlements infrastructure. What are the regulators’ concerns about public permissionless blockchain? Regulators often start from some assumptions that challenge the benefits or need for public permissionless blockchains. Essentially, because of the way regulation works in the traditional financial sector, this initial mistrust comes out of how different institutions and parts of the financial, regulatory and technology ecosystems look at the world. They see the words ‘public’ and ‘permissionless’ and conflate these with a lack of control over activities that should be regulated, and an inability to apply concepts like AML and KYC to participants. There’s a clash between worldviews. Are these concerns justified? A public blockchain typically isn’t a single application. It’s a network-based technology platform on which a range of applications and protocols can be built. These protocols themselves can have on-boarding requirements. Permissioning can also be implemented at the token level, so that tokens can only be transferred in accordance with predefined requirements. Nevertheless, public blockchains are increasingly recognizing the importance and value of supporting different permissioning mechanisms. Multichain blockchains, such as Avalanche and Cosmos, enable the creation of specialized blockchains, sometimes referred to as subnets or app-chains, that can be compliant by design. In these systems, developers can create chains with custom rule sets, execution environments, and governance regimes tailored to their needs. These custom blockchains unlock use cases previously not possible on blockchains with single rule sets, and isolate traffic and data into environments purpose-built for a given use case. They can also be natively interoperable with their mainnets and with other custom chains in the same network, enabling more of a balance to be struck between control and distribution of tokenized assets. Why go public and permissionless? Just as we don’t try today to control who has access to the internet and who can build on it, regulators and governments don’t need to try to control public blockchains to mitigate potential risks from them. They come with significant, in-built benefits in terms of robustness, security and resilience. Additionally, public and permissionless at the blockchain technology level is not synonymous with public and permissionless at the application level, and this is where regulators should focus their attention. There are many mechanisms available to implement robust compliance at the protocol and token level, while still benefiting from the network effects of a diverse, innovative ecosystem. As we’ve seen, there are valid use cases for both private, permissioned and public, permissionless blockchains, and both will continue to exist, and co-exist, into the future. Which one you use for your business will depend on the outcomes you wish to achieve, and how that aligns with the relative attributes of different blockchains. More and more actors both in the crypto space and traditional financial system are realising that public, permissionless blockchains can be a strong foundation for new ways of doing business.

DC Landscape as of January 28

Looking ahead, 2025 will be a pivotal year for blockchain, digital asset, and cryptocurrency-related legislative and regulatory policy across the Federal government. With Republicans now controlling both chambers of Congress and President Trump in the White House for a second term, this ‘trifecta’ will be integral in shifting the approach the United States takes towards policies impacting blockchain, cryptocurrencies, and other emerging financial technologies. Last year, the Financial Innovation and Technology of the 21st Century Act (FIT-21) was the first ever joint House Financial Services and Agriculture bill designed to bring some structure to the cryptocurrency market. It garnered bipartisan support in the House, with 71 Democrats voting for the bill, showcasing broader Democratic support for these issues. Stablecoin legislation also drew bipartisan and bicameral interest, which will continue to be a priority this Congress. Coupled by an unparalleled number of pro-digital asset candidates winning election or reelection to Congress, lawmakers will show–and already have shown a commitment to prioritizing these issues this year moving forward. Key Figures in Congress In Congress, the House Financial Services Committee and the Senate Banking Committee, as well as the House and Senate Agriculture Committees, are at the forefront of crafting policy surrounding digital asset regulation. Newly appointed House Financial Services Committee Chairman French Hill (R-AR) is known for his supportive stance on cryptocurrency and blockchain technology. Rep. Hill played a key role in the drafting, development, and ultimate passage of FIT-21 and will continue to advocate for policies that promote innovation in the digital asset space while ensuring consumer protection and market stability. We also expect him to align digital asset policies with the broader GOP agenda under the Trump Administration. With such tight margins in the House this year, Democratic support for any framework will also be necessary, as with FIT-21. Democratic Members on the Financial Services Committee, including Reps. Josh Gottheimer (D-NJ), Jim Himes (D-CT), and Richie Torres (D-NY), have been forward leaning on these issues and worked with the Majority to add amendments to the bill during mark-up. Ranking Member Waters (D-CA) had worked closely with former Chairman McHenry (R-NC) on stablecoin legislation in the last Congress including a last-minute push at the end of last year. That work will continue this year with Rep. Waters staying stablecoin legislation remains a top priority for her. With Republicans now controlling the majority in the U.S. Senate, Senate Banking Committee Chairman Tim Scott (R-SC) has already indicated he plans to move forward on digital asset issues and has created a new subcommittee on digital assets which will be chaired by Sen. Cynthia Lummis (R-WY), a longtime cryptocurrency and digital asset supporter. Senator Sen. Elizabeth Warren (D-MA) is the new Ranking Member of the Senate Banking Committee and has been vocal about her concerns with the industry over consumer protection issues and illicit finance and the need to regulate. However, in the 119th Congress the Committee will also include several newly appointed Democrats whose approach to policies in the crypto space are expected to differ from their Ranking Member. Senator Warren has named Senator Ruben Gallego (D-AZ) to be the Ranking Member of the Digital Assets Committee, showcasing an interest in having new Members take a leadership role on an important set of issues for the Committee. The House and Senate Agriculture Committee will also continue to be active on these issues as they were in the 118th Congress. The House Agriculture Committee, led by Chairman G.T. Thompson (R-PA), returned to his position and took a leadership role in working closely with the House Financial Services Committee on FIT-21, the first ever joint HFSC and Agriculture bill. The Committee has a new Ranking Member, Rep. Angie Craig (D-MN), who won a contested race amongst House Democrats to take over this role. In the Senate, Sen. Boozman takes over as the Chairman of the Agriculture Committee and with the retirement of former Sen. Stabenow (D-MI), Sen. Amy Klobuchar (D-MN) takes over as Ranking Member. Both have stated publicly they plan to fully engage on these issues and to work closely with the House Agriculture Committee. The Trump Administration: New AI/Crypto Czar and an Executive Order on Digital Assets In the White House, President Trump is taking a significantly different approach to digital assets compared to his first Administration. He has established a new position within the White House, appointing former PayPal executive David Sacks as the “AI and Crypto Czar.” This role is designed to spearhead the administration's efforts in the rapidly evolving fields of artificial intelligence and cryptocurrency. Sacks, a prominent venture capitalist and co-founder of an AI company, is expected to bring a pro-industry stance to the position, which aligns with the administration’s broader goals of fostering innovation and reducing regulatory barriers. On January 23, 2025, President Trump issued an Executive Order (EO) focusing on digital assets, stablecoins and CBDCs, entitled “Strengthening American Leadership in Digital Financial Technology.” The EO outlines the Administration’s policies on digital assets, financial technologies, and blockchain, such as ensuring open access to public blockchain networks, fair access to banking services, and prohibits any establishment of a CBDC. Notably, the EO establishes a working group within the National Economic Council to be chaired by Sacks to propose a federal regulatory framework for digital assets focusing on market structure, oversight, consumer protection, and risk management. The appointment of Sacks coincides with other significant changes in the regulatory landscape, such as the anticipated confirmation of Paul Atkins to be Chairman of the SEC. Atkins’ predecessor, Gary Gensler, took a very aggressive ‘regulation by enforcement’ approach to emerging digital assets. This alignment suggests a concerted effort by the administration to overhaul existing policies and focus on clearer guidance to industry on how the SEC views securities in the digital assets and cryptocurrency industry. Soon after being named Acting Chair, Commissioner Mark Uyeda announced the creation of a crypto task force dedicated to developing a comprehensive and clear regulatory framework for crypto assets. Under Uyeda, the SEC has already rescinded Staff Accounting Bulletin 121, which created onerous reporting requirements on banks and crypto companies. Legislative Focus on Blockchain and Fintech The House Financial Services Committee, under Chairman Hill’s leadership, is expected to work on policies that integrate digital assets into the broader financial system, while also potentially addressing regulatory clarity and consumer protection. Both the House Financial Services Committee and the House Agriculture Committee have indicated that they will focus on updating FIT-21, working with industry and the new Trump Administration, all of which will be a primary focus in the first six months of the year. Meanwhile, the Senate Banking Committee, led by Sen. Scott, aims to champion legislative changes that support the crypto industry's growth, addressing concerns about innovation being stifled by existing regulations. Stablecoin legislation, which had bipartisan support in the House is likely to be moved more quickly early in 2025, while efforts will continue on updating FIT-21. The collaboration between Congress and Administration officials will be crucial in shaping a comprehensive approach to fintech and digital assets. While the legislative efforts will likely focus on creating a balanced regulatory environment that fosters innovation and includes consumer protection issues while ensuring the stability and security of the financial system; the Administration is likely to focus on issues such as the SEC and the CFTC working in lockstep with Congress to pass a legislative and regulatory framework for digital assets that includes consumer protections and clearer “rules of the road.” This alignment and a broader focus by more Members in a bipartisan and bicameral fashion appear to showcase an optimistic 2025 for consumers and the industry. Authors: Norma Krayem (VP & Chair, Cybersecurity, Privacy and Digital Innovation, Van Scoyoc Associates) Scott Mason (Senior Policy Advisor at Holland & Knight LLP)

and Scott Mason

A Primer: Understanding Tokenized Real-World Assets

A Primer: Understanding Tokenized Real-World Assets by: Lilya Tessler (Partner), Andrew Sioson (Partner), and Erika Cabo (Senior Managing Associate) at Sidley Austin, LLP Tokenization of real-world assets (RWAs) is revolutionizing the way we perceive and manage assets. This article aims to provide an overview of RWAs, debunk common myths, and outline the legal considerations and risks associated with tokenized RWAs. What Are Tokenized RWAs? The term “tokenized RWAs” refers to the digital representation of physical or intangible assets utilizing a token recorded on a blockchain. This innovative approach allows for the efficient recording, trading, transferring, and management of tangible assets in a digital format. A wide range of RWAs can be tokenized, including real estate, commodities, art, and intellectual property. By recording ownership of these assets using digital tokens, they can be more easily tracked and traded on blockchain platforms. This is similar to the e-commerce trend in the 1990s, when online shopping sites were developed to allow consumers to buy physical goods by seeing digital images on the internet, instead of physically going to a brick-and-mortar store in a shopping mall to see, feel, and buy the items. The primary benefits of tokenizing real-world assets include increased liquidity, fractional ownership, and enhanced transparency. Tokenization allows for the division of assets into smaller, more affordable units, making it easier for a broader range of purchasers to participate. Additionally, the use of blockchain technology ensures a transparent and immutable record of ownership and transactions. Debunking Myths: Tokenized Assets vs. TGEs and STOs Tokenization is not a new concept. Digital records have existed for years from digital shopping sites, digital concert tickets, and digital securities. Tokenization of RWAs is simply recording these digital records on a blockchain as opposed to other centralized databases. Tokenizing an asset does not change the nature of the asset and it is not to be confused with token generation events (TGEs) or security token offerings (STOs). Below are some of the common myths regarding asset tokenization that need to be clarified. Myth 1: Tokenizing an Asset Changes the Nature of the Asset Tokenizing an asset does not change the nature of the asset itself. Tokenization is the process of creating a digital representation of a physical or intangible asset using a token recorded on a blockchain. This digital token serves as a record of ownership and can be traded or transferred on blockchain networks. However, the underlying asset remains the same, whether it is real estate, art, commodities, or intellectual property. The token merely provides a more efficient and transparent way to manage and transfer ownership of the asset, without altering its fundamental characteristics or value. Myth 2: Tokenized Assets Are TGEs TGEs are a mechanism used by new blockchain protocols to distribute tokens to potential users of the network. These tokens, such as ETH (Ethereum) and AVAX (Avalanche), are designed to provide functionality within the blockchain ecosystem, enabling users to interact with the network, pay for services, or validate transactions, among other uses. TGEs are not a form of fundraising, but they are also not tokenized RWAs, because the token associated with the TGE represents utility on the network and not a digital representation of an actual asset. In contrast, tokenized RWAs are digital representations of actual, tangible, or intangible assets. The value of these tokenized RWAs is directly linked to ownership of the underlying assets, which can be verified and audited. Myth 3: Tokenized Assets Are Just Another Form of STOs STOs involve the issuance of tokens that are classified as securities and are subject to regulatory oversight. These tokens are backed by assets that generate income or have equity-like features, such as dividends, voting rights, or profit sharing. Although tokenized RWAs can be tokenized equity or fund interest, they are not limited to securities and have many more benefits when representing a wide range of other physical or intangible assets. The primary focus of tokenized RWAs is on the digital representation and fractional ownership of these assets, rather than raising capital through the issuance of securities. Legal Considerations Regulatory Compliance: Navigating the regulatory landscape is crucial for tokenized RWAs. Compliance with U.S. securities and commodities laws, anti-money laundering regulations, commercial laws, and know-your-customer requirements is essential to ensure the legality and legitimacy of tokenized assets. Ownership and Transfer of Title: The digital representation of an asset must accurately reflect the legal ownership of the holder and their enforceable right to the underlying asset. Ensuring clear and enforceable ownership rights is critical to the success of tokenized RWAs. Smart Contracts: Smart contracts are self-executing agreements encoded on the blockchain and triggered by predefined conditions. While they play a vital role in automating and streamlining the tokenization process, one must consider whether smart contracts are enforceable, comply with existing contract laws and regulations, and adequately address potential disputes and contingencies. Jurisdictional Issues: Tokenized assets can be created and traded globally, raising questions about cross-border jurisdiction and applicable laws. Being aware of the roles of regulatory bodies such as the U.S. Securities and Exchange Commission, U.S. Commodity Futures Trading Commission, European Securities and Markets Authority, Monetary Authority of Singapore, Hong Kong Monetary Authority, and others globally is of paramount importance in navigating different legal frameworks and standards for tokenization. Risk Considerations and Management Security Risks: Blockchain technology is not immune to cybersecurity risks, such as hacking, phishing, or malware attacks. Tokenized assets may be vulnerable to theft, loss, or manipulation if the private keys, wallets, or platforms that store and access them are compromised. Ensuring the security and integrity of the blockchain and the tokenized assets is paramount to protecting investors and maintaining trust in the system. Market Risks: Tokenized assets are subject to market volatility and liquidity risks, depending on the supply and demand of the tokens and the assets, as well as the performance and stability of the blockchain platforms. Considering risk mitigation strategies is essential in order to protect investments and navigate the complexities of the tokenized asset market. Conclusion Tokenized RWAs represent a significant advancement in the management and trading of physical and intangible assets. They can unlock new value, efficiency, and innovation for both asset owners and investors. However, they also pose significant legal challenges and risks that need to be addressed and managed. Seeking guidance from law firms on regulatory compliance, ownership issues, and risk management, while engaging with experienced vendors and blockchain platforms, can provide the necessary technical knowledge and support to ensure the smooth operation of tokenized RWAs. As the landscape continues to evolve, staying informed and proactive will be key to leveraging the full potential of tokenized RWAs.

and Erika Cabo

and Andrew Sioson

‘Crafting The Crypto Economy’ Series Returns With Academic and Legal Thought Leaders

Audio show ushers in a new and necessary storytelling format for navigating the world of Web3, exploring themes of privacy, regulatory compliance, niche markets makers, and decentralized exchange ecosystems in blockchain. Web3 policy-focused podcast, Owl Explains, returns for a second season of ‘Crafting The Crypto Economy’ with leading academics to tackle timely regulatory challenges and the practical blockchain applications reshaping Web3. Focusing on critical topics from Decentralized Exchanges (DEXes) regulation, blockchain privacy, and MEV mitigation, ‘Crafting The Crypto Economy’ introduces academic thoughtleaders and papers from around the world with the latest research on blockchain technology and the crypto economy. With five substantive episodes, Season 2 drops in with well-timed topics to equip policymakers and stakeholders with valuable insights on Web3 regulation and emerging challenges. The hosts of this series, Professors Andreas Park (University of Toronto) and Fahad Saleh (University of Florida) are leading authors in Blockchain Economics and Finance and are part of the Crypto and Blockchain Economics Research (CBER) Forum. The group producing the podcast, Owl Explains, is a trusted blockchain policy resource driven by the expertise of Ava Labs’ Legal team. This partnership between Owl Explains and the CBER Forum seeks to bridge the gap between academic rigor and actionable insights for policymakers. As the SEC increasingly scrutinizes decentralized finance (DeFi) platforms, Episode 1, ‘Regulation of Decentralized Exchanges,’ with Professors Campbell Harvey of Duke University and Joel Hasbrouck of NYU Stern, dives into the novel risks for traders who trade at DEXes and why standard regulatory approaches are not well-suited for addressing those risks. In Episode 2, ‘Blockchain Privacy and Regulatory Compliance,’ Professor Fabian Schär from the University of Basel discusses how blockchain users may attain privacy in their transactions while also remaining compliant. Despite the perception of anonymity, most blockchain transactions are traceable, leading to a rising demand for privacy solutions. The episode explains how blockchain identities are not anonymous and what methods may be implemented to achieve both privacy and regulatory compliance. Detailing the economic values presented in the concepts of Maximal Extractable Value (MEV) and Loss-Versus-Rebalancing (LVR), Columbia University’s Professor Ciamac Moallemi discusses associated mitigation methods such as expedited block times and auction mechanisms for extraction in ‘Mitigation Methods for MEV and LVR.’ Moving into intent-based markets (i.e., Uniswap X, CoW Swap) as a hot topic, ‘Decentralized Exchange (DEX) Aggregators and Solvers,’ with Professor Mallesh Pai of Rice University, explores the economic implications of these niche markets, potential outcomes for traders, and the impact of their underlying economic structures. The World Economic Forum predicts that 10% of global GDP will be tokenized on the blockchain by 2027. Wrapping up the Season 2, ‘Deep-dive on the Avalanche Blockchain’ features Ava Labs’ Chief Protocol Architect Stephen Buttolph to discuss how Avalanche’s blockchain can be used for the tokenization of real-world assets, specifically through the lens of Avalanche’s consensus protocol. Owl Explains and the CBER Forum are committed to helping regulators navigate the world of Web3 and break through the hype. In an always-on blockchain landscape, ‘Crafting The Crypto Economy’ breaks through the noise, leveraging curated perspectives and mental models from top minds in the space.

Building Bridges in Blockchain Policy – Our Growing US Congress Series

At Owl Explains, we believe the future of blockchain and crypto lies in the conversations happening today between industry leaders and policymakers. That’s why our Congress Series is dedicated to bringing you the sharpest voices in US policy, offering insights on the regulatory and legislative shifts shaping the blockchain landscape. From bipartisan collaboration to bold individual initiatives, our guests tackle the tough questions about self-custody, tokenization, and market structure clarity. These are the policymakers from both at the heart of the debate—ready to share their vision for the role of blockchain in America’s economic future. Meet the Voices of Change: Ep. 17: Congressman Mike Flood Kicking off with Rep. Mike Flood, this episode takes a close look at the difference in perspectives on crypto policy between the House and the Senate and how Congress can build momentum for lasting change. Ep. 32: Congressman French Hill Rep. French Hill shares his take on bipartisan efforts to move blockchain forward, touching on key themes like self-custody and market clarity. Ep. 30: Congressman Wiley Nickel As the political landscape evolves, Rep. Wiley Nickel brings fresh perspective to the table, discussing tokenized markets and their potential to boost US innovation. Ep. 35: Congressman Shri Thanedar (D-MI-13) Rep. Shri Thanedar explores blockchain’s potential to create equity and opportunity, focusing on how technology can drive meaningful policy change. Ep. 36: Congresswoman Yadira Caraveo (D-CO-08) Colorado’s Congresswoman Yadira Caraveo examines the intersection of policy and technology in her state, emphasizing the potential for decentralized systems to support local economies. Ep. 40: Congressman Dusty Johnson (R-SD) Rep. Dusty Johnson offers a refreshing take on blockchain’s role in rural America, highlighting how innovation isn’t just for Silicon Valley. Ep. 42: Congressman Warren Davidson (R-OH-08) Rep. Warren Davidson doesn’t shy away from the big issues—self-custody, tokenization, and why market structure clarity is critical for the U.S. to reclaim its crypto leadership. A Growing Series, A Growing Dialogue As the Congress Series grows, so does the urgency of the topics at hand. Whether it's legislation like the FIT21 Act, the fight to protect self-custody, or debates on token taxonomy, these episodes are more than conversations—they’re a front-row seat to the policies that will define blockchain’s future in America. Cryptocurrency and blockchain technology are rapidly transforming the global economy. As these technologies become more widely adopted, governments are increasingly grappling with how to regulate them. Crypto policy is important because it will shape the future of the crypto industry and its impact on society. The United States is at the forefront of the global crypto policy debate. At Owl Explains, we’re proud to bring together voices from both sides of the aisle to discuss solutions, challenges, and the road ahead. The series is just getting started, and there’s so much more to come. Catch up on the Congress Series today and hear directly from the policymakers shaping the future of crypto, on Spotify, Apple Podcasts, or right here in our owl website.

A Huge Thank You to Our Incredible Sponsors - Avalanche Summit LATAM 2024

As we gear up for the Avalanche Summit LATAM 2024, we want to take a moment to express our deepest gratitude to the sponsors who have made this event possible. Their support empowers us to bring together the brightest minds in the blockchain, crypto, and Web3 space for meaningful discussions, collaborations, and innovation. We are thrilled to partner with these visionary companies and organizations, each playing a vital role in pushing the boundaries of what's possible in the Web3 world. Without further ado, we’d like to introduce our valued sponsors: Platinum Owl Sidley Austin LLP Golden Owls Cleary Gottlieb Steen & Hamilton Davis Polk & Wardwell Sher Tremonte Boreal Owls Fenwick Latham & Watkins Willkie Farr & Gallagher LLP Snowy Owl HJF Law Community Partner Global Blockchain Business Council Our sponsors are more than just logos on our website—they are leading law firms, trade associations, and innovators who share our passion for decentralization, transparency, and the transformative power of blockchain technology. What's on the Agenda? The Best of Buenos Aires! Imagine this: a summit filled with cutting-edge discussions, hands-on workshops, and networking opportunities with some of the brightest minds in blockchain, all set in the dynamic, bustling city of Buenos Aires. From exploring the iconic streets of San Telmo to the modern vibe of Puerto Madero, the Avalanche Summit is going to be an event that brings together innovation and the unique spirit of Argentina, Latin America, and beyond! 🇦🇷✨ And let’s not forget the local flair! From delicious Argentine cuisine (empanadas, anyone? 🥟) to the vibrant street art that colors the city, we’re blending tech with culture in a way only Buenos Aires can. To our sponsors—thank you for believing in this vision and helping us make it happen. Your support is turning this event into a groundbreaking moment for the Web3 community in LATAM. We can’t wait to see what we’ll achieve together! So, let’s give a big round of applause to these amazing partners and look forward to meeting up in Buenos Aires, where the future of blockchain is being written, one tango step at a time! 🎵 Get your tickets for 50% off using our code OWL50.

Custom Blockchains: Shaping a Bespoke Future

The inception of blockchain technology, heralded by Satoshi Nakamoto's whitepaper on Bitcoin, ignited a revolution whose full magnitude is only now coming to light. Yet, the true marvel doesn't lie solely in the foundational concept outlined in 2008; it resides in the ongoing evolution, fueled by brilliant minds since. Today, we stand on a new frontier: customization. Picture a world where launching a tailored blockchain, precisely attuned to your requirements, is not just a possibility but a reality. Custom blockchains represent an evolution from the original Satoshi blueprint; they embody vibrant ecosystems full of innovation. This newfound flexibility empowers users to design blockchains endowed with specific features and functionalities. The result? New applications and diverse use cases. Consider the foray of Sports Illustrated into blockchain technology, where sports fans securely purchase and trade verified tickets to their favorite events, all facilitated by a custom blockchain engineered for authenticity and transparency. This reality, where tickets unlock immersive experiences and collectibles, is not a distant dream but a tangible outcome crafted by forward-thinking enterprises. Similarly, Lemonade's* disruption in the insurance industry depicts the transformative potential of custom blockchains. Through their tailored solution, they've revolutionized weather insurance for small farmers, providing a seamless and transparent shield against unpredictable climate events. This paradigm shift underscores blockchain's role as a tangible force for positive change, far beyond mere rhetoric. The collaboration between Deloitte and FEMA** on disaster recovery reimbursement offers yet another glimpse into the power of custom blockchains. By leveraging blockchain technology, they've streamlined the reimbursement process, ensuring timely and transparent aid to those affected by disasters while simplifying audits. It's a compelling illustration of blockchain's capacity to enhance efficiency and accountability in critical domains. When it comes to loyalty programs and gaming, SK Global’s custom blockchain platform is at the vanguard of innovation. Their solution enables millions of South Korean telecom customers to use loyalty points across thousands of merchants, from real-world items to digital goods, with confidence in the authenticity and scarcity of their digital assets. This convergence of ecosystems and commerce, powered by blockchain technology, illuminates a path towards a more secure and transparent future for consumers and merchants alike. Even traditional financial institutions are embarking on the era of custom blockchains, with giants like Citi and JPM exploring the potential to trade traditional financial assets on custom platforms. This transition promises enhanced efficiency, transparency, and security in the financial landscape, marking a significant stride towards mainstream blockchain adoption. Whether revolutionizing real estate transactions, enhancing supply chain visibility, or reimagining loyalty programs, the space for innovation is extensive. What if we could tailor our digital ecosystems to align with our needs and aspirations? While some headlines may dwell on the volatility of cryptocurrencies, the true narrative lies in the transformative power of blockchain technology. We’re all about more hoot and less hype and recognize the capabilities of custom blockchains as canvases where creativity flourishes and ideas find their specific homes. It's time for Washington, and the world at large, to recognize custom blockchains as catalysts for innovation, efficiency, and inclusion across industries. *Lemonade's use case: *Lemonade's use case: **Deloitte and FEMA: **Deloitte and FEMA: